You're not just considering buying a business.

You're setting the price you'd pay for it.

Two businesses in the same price range can deserve very different numbers — one priced like a well-equipped Toyota, the other like a base Lexus. The CIM won't tell you which lot you're standing in. What the business can actually stand on without the person selling it will.

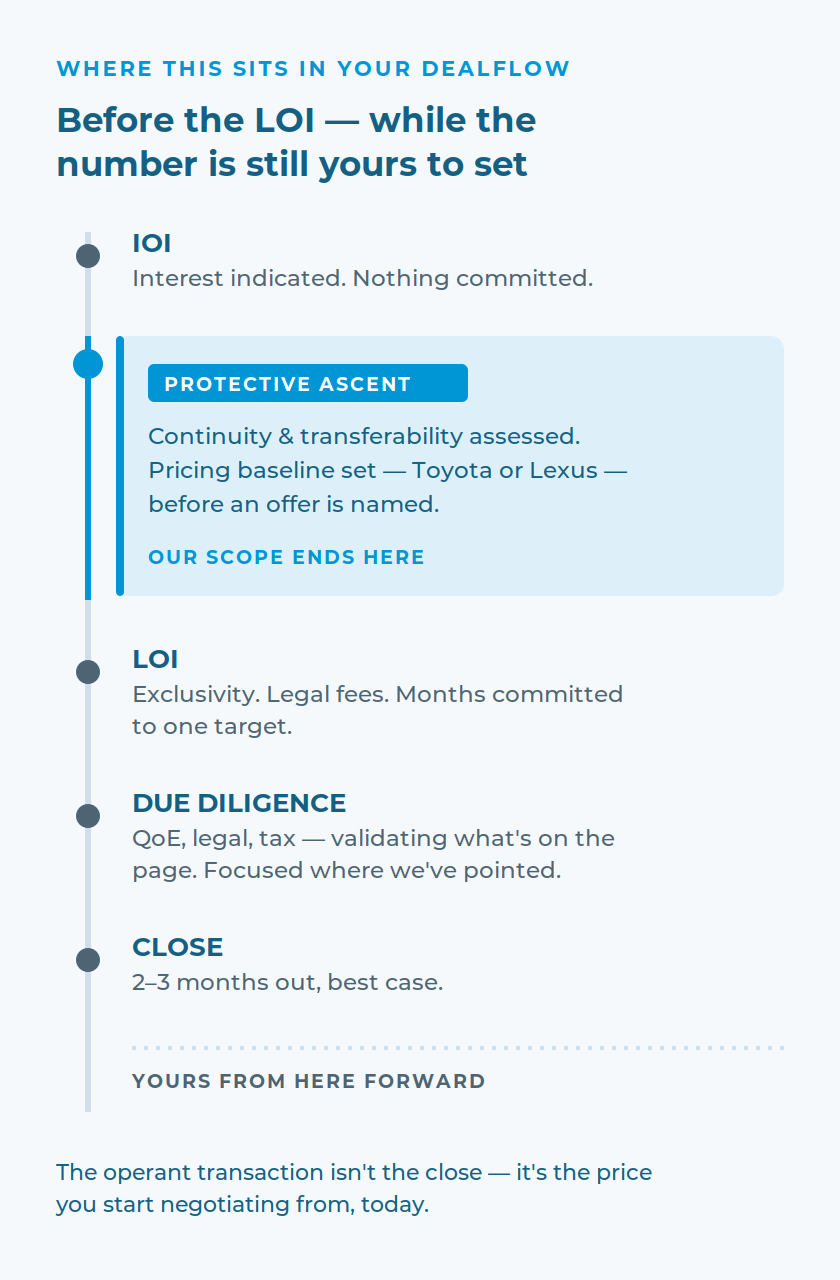

Protective Ascent is a pre-LOI, buyer-side assessment of continuity and transferability for lower-middle-market acquisitions — built to set that pricing baseline before you make an offer.

- A supplement to Quality of Earnings — not a replacement for it, or for due diligence

- Focused on what QoE and legal review aren't built to make central: whether the business runs on its own, or runs on the person selling it.

"If this is one deal, a bad surprise is a bad quarter. If it's the fifth deal this year, it's a pattern in the portfolio."

The operant transaction isn't the close — it's the price you start negotiating from, today. Post-LOI diligence can surface transferability issues, but usually as a byproduct of financial or legal review rather than the focus. This asks the question directly, on purpose — and puts the answer in your hands before you've named a price.

The Question your Diligence isn't Built to Ask

You've been through the CIM. Maybe you've already got a QoE provider lined up, or legal counsel reviewing contracts. That's the diligence everyone tells you to do — and you should still do it. But none of that is built to make this the primary question:

What's driving you to want to understand what actually continues to function once the seller is out of the picture?

Whether the pricing decisions run through one person's head. Whether the biggest customer trusts the company, or trusts the owner personally. Whether the team can actually run the place on day 31 without a phone call to someone who no longer works there. Standard diligence might stumble onto pieces of this. It isn't built to go looking.

This isn't a sign the business is poorly run — plenty of great businesses operate this way. It's a sign you need to know whether it's a factor before you decide what this is worth to you.

WHAT THAT COSTS WHEN YOU FIND IT LATE

Discovery findings, not line items

Customer relationships belong to the seller, not the business

The CIM said: "strong customer relationships." It didn't say with whom. Lost revenue, delayed value creation, and cascading retention effects as departing accounts talk to deciding ones.

$100K+

SIX FIGURESKey people were loyal to the seller, not the business

Direct spend on consultants, outsourcing, hiring, and training — plus every month spent backfilling instead of building. One departure can be absorbed. Multiples get dangerous. Across a portfolio, multiples become a pattern.

$100K–$1M+

SIX-TO-SEVEN FIGURESThe business is at capacity, with no systems to ramp

Uncommon, but it happens — and it can break the value thesis outright. When findings point here, the honest recommendation may be to walk away before the LOI, and we consult with you directly on that decision.

$1M+

SEVEN FIGURESWhat It Is — And Isn't

A Supplement to your Diligence, not a Substitute for it

This is not

- Quality of Earnings

- Financial due diligence

- Legal or tax diligence

- Cybersecurity or technical diligence

- Commercial diligence

- EBITDA recalculation or add-back validation

- A valuation

This is

- Leadership Dependency — what stops when the seller leaves

- Knowledge Concentration — what lives only in someone's head

- Relationship Concentration — whose relationships these really are

- Decision Rights Mapping — distributed & documented or centralized & informal

- Management Depth — who leads when the seller isn't in the room

- Process Transferability — whether workflows survive the ownership change

The Experience Behind the Read

20years leading integration & transformation | 14industries |

$140Mnet-new value created for clients |

50+initiatives led, discovery through execution |

I developed the S.C.O.R.E. framework as the backbone of how that value gets identified, qualified, and translated to my clients.

Across resistant acquisitions, departments, and institutions, I learned to draw the truth out of the hiding, the hedging, the protective, the confident-but-mistaken, and the genuinely unaware. The point is to get to the core issues that can make or break an effort. Having come up through analysis before leading stakeholders and executives, I know how to speak to an audience in a way that invites them to reveal the truth rather than putting them on the defensive.

From there, I translate those findings — combined with deep knowledge of business systems and capabilities — into two distinct reads.

First, what will transfer cleanly through the transition and what won't — surfacing where Enterprise Value deserves a second look. Not a number, but a clear-eyed sense of what the business is actually worth once you separate what's transferable from what was riding on the seller.

Second, what's a foundation the business can be built on as currently configured, and what will need to be rebuilt first — the core of what drives Time-to-Playbook.

Together, those two reads answer the question that matters most before you name a number: whether you're standing in front of a Lexus, or a Toyota wearing a Lexus price tag.

Picture the Other Side

Picture walking into the first real conversation about price already knowing which lot you're standing in — Toyota money or Lexus money — instead of hoping the CIM's number holds up once someone starts asking harder questions. You've already seen where the shine is real and where it's lipstick, before spending the time, cost, and energy of full due diligence finding out for yourself.

That's the immediate value: a baseline you can stand behind before you've named a number. What happens after that — if the deal moves forward — is real too, but it's downstream. Whatever diligence still needs to happen is aimed at the specific areas that need a harder look, not a blanket search for problems you don't have a name for yet. The 100-day plan runs the way it's written because it was built on what the business actually is, not what the CIM said it was. Value creation starts on day one instead of month four spent rediscovering the business you bought.

And if you're running more than one deal a year, this compounds. A pricing baseline you can set the same way every time isn't just protection on this deal — it's discipline you carry into the next one, and the one after that. Surprises stop being a cost of doing deals and start being a solved problem in your process.

What's actually different for you and your team walking into an offer with that baseline already set?

That's not an abstract efficiency gain. It's a confident read on the price you should be negotiating from — before the negotiation starts.

Why does that matter to you and your team, specifically, on this deal?

Deliverables

What You Get

- Operational Continuity Assessment — a narrative read on continuity risk: what's strong, what's concerning, what's genuinely fragile

- Continuity Risk Register — a prioritized list of the specific vulnerabilities found (knowledge concentration, relationship concentration, authority bottlenecks, and so on)

- Day-One Vulnerability Assessment — where the business would need to prove itself immediately after close

- Time-to-Playbook Considerations — how much runway the business needs before it performs the way the CIM implies

- Knowledge Transfer Priorities — what's currently living in one person's head instead of the business